As India’s salaried workforce plans for retirement amid rising life expectancy and inflationary pressures, the Employee Provident Fund (EPF) and its linked pension scheme remain central to long-term financial security. By 2026, the debate around “higher pension” under the Employees’ Pension Scheme (EPS), administered by the Employees’ Provident Fund Organisation (EPFO), has become one of the most consequential issues for organised-sector employees and retirees. Following a series of court rulings, administrative clarifications, and implementation exercises over the past few years, employees are seeking clarity on how pensionable salary is calculated, who is eligible for higher pension benefits, and what the rules practically mean for monthly retirement income.

Background: Understanding EPF and EPS in the Indian system

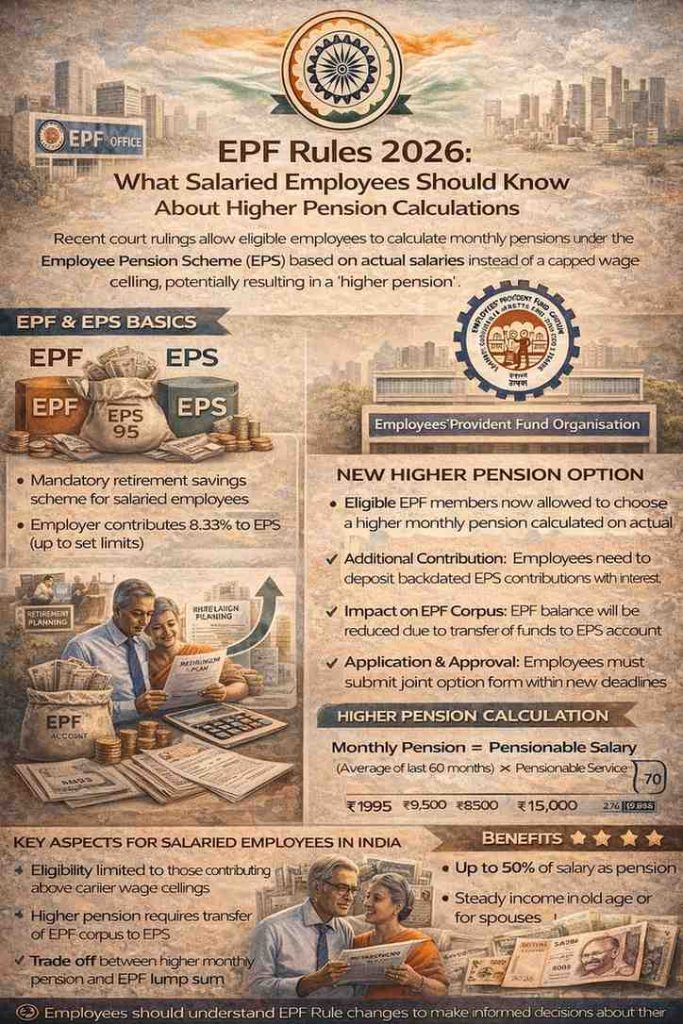

The EPF is a statutory retirement savings scheme governed by the Employees’ Provident Funds and Miscellaneous Provisions Act, 1952. It applies to most establishments in the organised sector and is mandatory for employees earning up to a specified wage threshold at the time of joining, though higher-paid employees may also continue under certain conditions.

Under the EPF framework, contributions are split between the provident fund and the pension scheme. Employees contribute a fixed percentage of their basic salary and dearness allowance, matched by the employer. Of the employer’s contribution, a portion is diverted to the Employees’ Pension Scheme, 1995 (EPS-95), which provides a defined-benefit pension upon retirement, subject to eligibility conditions such as minimum years of service.

For decades, pension calculations under EPS were based on a statutory wage ceiling rather than actual salary. This ceiling, which has changed over time, limited the pensionable salary used to compute monthly pension payouts. As a result, even employees who contributed on higher salaries often received pensions calculated on the capped amount.

The long-standing issue of wage ceiling and pension calculation

The concept of a wage ceiling has been at the heart of disputes around EPS. Historically, the ceiling was set at relatively low levels compared to actual salaries in many sectors. While employees and employers could opt to contribute to EPF on higher wages, pension contributions under EPS were generally restricted to the notified ceiling unless specific options were exercised.

This created a disconnect. Employees who contributed substantial amounts to EPF over long careers found that their pension under EPS was modest, reflecting the capped pensionable salary rather than their real earnings. Over time, this disparity led to legal challenges by employees seeking pension calculation based on actual salary.

Judicial interventions and their significance

The issue reached the courts multiple times, culminating in a landmark Supreme Court judgment in November 2022. The court upheld the right of eligible employees to opt for higher pension based on actual salary, subject to compliance with the scheme’s provisions. At the same time, the court recognised the administrative and financial implications for the EPFO and allowed for a structured implementation process.

The judgment clarified that employees who were members of EPS before the introduction of the higher wage ceiling in 2014, and who had contributed to EPF on salaries exceeding the ceiling, could exercise a joint option with their employer to have pension calculated on actual salary. It also acknowledged that additional contributions would be required, reflecting the difference between earlier capped contributions and those based on higher wages.

Administrative implementation and evolving timelines

Following the Supreme Court ruling, EPFO issued circulars outlining the process for exercising the higher pension option. These included deadlines for submitting joint options, verification of records, and recalculation of pensionable service and salary. The process was complex, involving coordination between employees, employers, and EPFO field offices.

Deadlines for submitting options were extended multiple times to accommodate practical difficulties, such as lack of historical wage records or non-cooperation from defunct employers. By the mid-2020s, a significant number of applications had been received, but processing remained uneven across regions.

As of 2026, higher pension under EPS is not a new scheme but an outcome of judicial interpretation of existing rules. There has been no overhaul of the EPS framework; rather, the focus has been on implementing the court’s directions within the existing statutory structure.

What “higher pension” actually means

Higher pension refers to the calculation of monthly pension based on actual pensionable salary, rather than the statutory wage ceiling, for eligible employees. Under EPS, pension is calculated using a formula that takes into account pensionable salary and pensionable service.

For employees whose pensionable salary is recalculated upwards, the resulting monthly pension can be substantially higher than what would have been payable under the capped system. However, this increase is not automatic or universal. It depends on factors such as length of service, level of salary, and the amount of additional contribution required.

Eligibility criteria as understood by 2026

By 2026, the broad contours of eligibility have become clearer through administrative practice. Employees who were members of EPS prior to September 2014 and who contributed to EPF on salaries exceeding the wage ceiling during their service period are generally considered eligible to apply for higher pension. The presence of a joint option, explicit or implicit, has been a key factor in determining eligibility.

Employees who joined EPS after the 2014 amendment, which raised the wage ceiling and introduced additional conditions, face more restrictive rules. For this group, pensionable salary is generally capped at the notified ceiling, and the option for higher pension is limited.

Retired employees are also eligible under certain conditions, though the recalculation of pension involves adjustments to past contributions and, in some cases, recovery of additional amounts.

Financial implications for employees

One of the most significant aspects of higher pension is the requirement to contribute additional funds. Since EPS contributions in the past may have been made on a capped salary, employees opting for higher pension must make up the difference between what was contributed and what should have been contributed based on actual salary.

This adjustment can involve substantial sums, especially for employees with long service and high salaries. The EPFO has allowed for adjustment of amounts from the employee’s provident fund balance in many cases, reducing the need for out-of-pocket payments. However, this also means a lower lump-sum EPF corpus at retirement, creating a trade-off between monthly pension and accumulated savings.

Impact on monthly pension payouts

For those who successfully opt for higher pension, the impact on monthly income can be significant. A recalculated pension based on actual salary and full pensionable service can result in multiples of the earlier pension amount. This is particularly relevant for retirees who rely heavily on pension as a stable source of income.

However, it is important to note that EPS pensions are not indexed to inflation. While the initial pension amount may be higher, its real value may erode over time unless supplemented by other retirement income sources.

Administrative and actuarial challenges for EPFO

The implementation of higher pension has posed challenges for the EPFO. Recalculating pension for large numbers of employees requires verification of decades-old wage records, reconciliation of contributions, and coordination with employers, some of whom no longer exist.

From an actuarial perspective, higher pension payouts increase the long-term liabilities of the pension scheme. EPS is a defined-benefit scheme funded through contributions and managed by EPFO. Ensuring its financial sustainability while honouring higher pension commitments remains an ongoing concern.

By 2026, EPFO has continued to emphasise careful scrutiny of applications and phased implementation to manage these challenges.

Implications for current salaried employees

For employees still in service, the higher pension issue underscores the importance of understanding contribution structures early in one’s career. Decisions about contributing on higher wages, maintaining proper documentation, and tracking EPF and EPS records can have long-term consequences.

Employees nearing retirement face more immediate choices. Opting for higher pension may make sense for those prioritising steady monthly income, while others may prefer to preserve a larger EPF corpus for flexibility and bequest planning.

Employer responsibilities and practical constraints

Employers play a crucial role in the higher pension process. Joint options require employer certification of wage details and contribution history. In cases where employers are uncooperative or records are incomplete, employees face delays or rejection of applications.

Large organisations with well-maintained payroll systems have generally been better positioned to support employees. Smaller establishments and those that have closed down present more complex scenarios, often requiring intervention by EPFO authorities.

Communication gaps and employee awareness

Despite widespread media coverage, awareness about the technical details of higher pension remains uneven. Many employees misunderstand eligibility conditions or overestimate potential benefits without accounting for required adjustments.

By 2026, EPFO has increased outreach through circulars and online portals, but the complexity of the subject means that employees often rely on professional advice. Clear communication remains a challenge, particularly for retirees and employees in smaller towns.

Interaction with broader retirement planning

Higher pension under EPS should be viewed as one component of a broader retirement strategy. EPF accumulations, voluntary provident fund contributions, National Pension System investments, and personal savings all interact to determine post-retirement financial security.

The choice between a higher monthly pension and a larger lump sum reflects individual preferences, health considerations, family responsibilities, and alternative income sources. There is no uniform answer applicable to all employees.

Policy debates and future outlook

The higher pension issue has also sparked broader debates about the design of India’s pension systems. Defined-benefit schemes like EPS offer predictability but pose sustainability challenges, while defined-contribution schemes shift risk to individuals.

As of 2026, there has been no formal announcement of structural reform to EPS. Policymakers appear focused on implementing existing legal directions rather than redesigning the system. However, discussions around long-term pension adequacy and fiscal sustainability continue in policy circles.

What employees should realistically expect in 2026

For salaried employees and retirees, 2026 represents a phase of consolidation rather than change. The legal position on higher pension is settled, but administrative processing continues. Employees who are eligible and have applied may still be awaiting final decisions, while others must accept that eligibility is limited by statutory timelines and service conditions.

Those considering retirement planning should factor in realistic timelines for pension recalculation and avoid assuming immediate or automatic increases.

Conclusion

The evolution of higher pension under the Employee Provident Fund framework reflects the complex interplay between law, policy, and individual retirement needs. By 2026, the contours of the issue are clearer than in the immediate aftermath of court rulings, but practical challenges remain.

For salaried employees, understanding EPF and EPS rules, particularly around pensionable salary and service, is essential for informed decision-making. Higher pension can offer meaningful financial security for some, but it comes with trade-offs that must be carefully weighed.

As India’s workforce continues to change and longevity increases, the conversation around pensions is likely to intensify. The experience of implementing higher pension under EPS serves as a reminder that retirement policy is not just about numbers, but about balancing fairness, sustainability, and the diverse needs of millions of employees.

Add newsproton.com as preferred source on google – click here

Last Updated on: Thursday, January 29, 2026 12:11 pm by News Proton Team | Published by: News Proton Team on Thursday, January 29, 2026 12:11 pm | News Categories: India